Cash Cycle Coordination for Boutique Subscription Providers Using Multi-Rail Payment Strategies

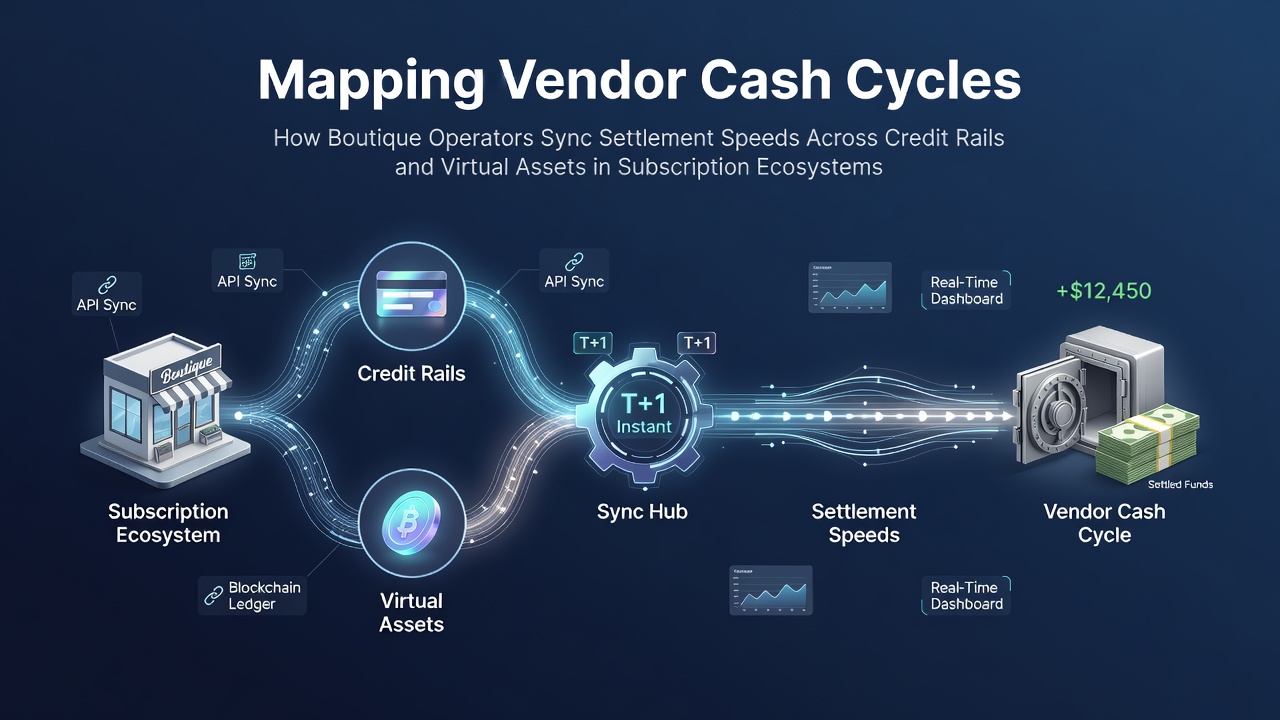

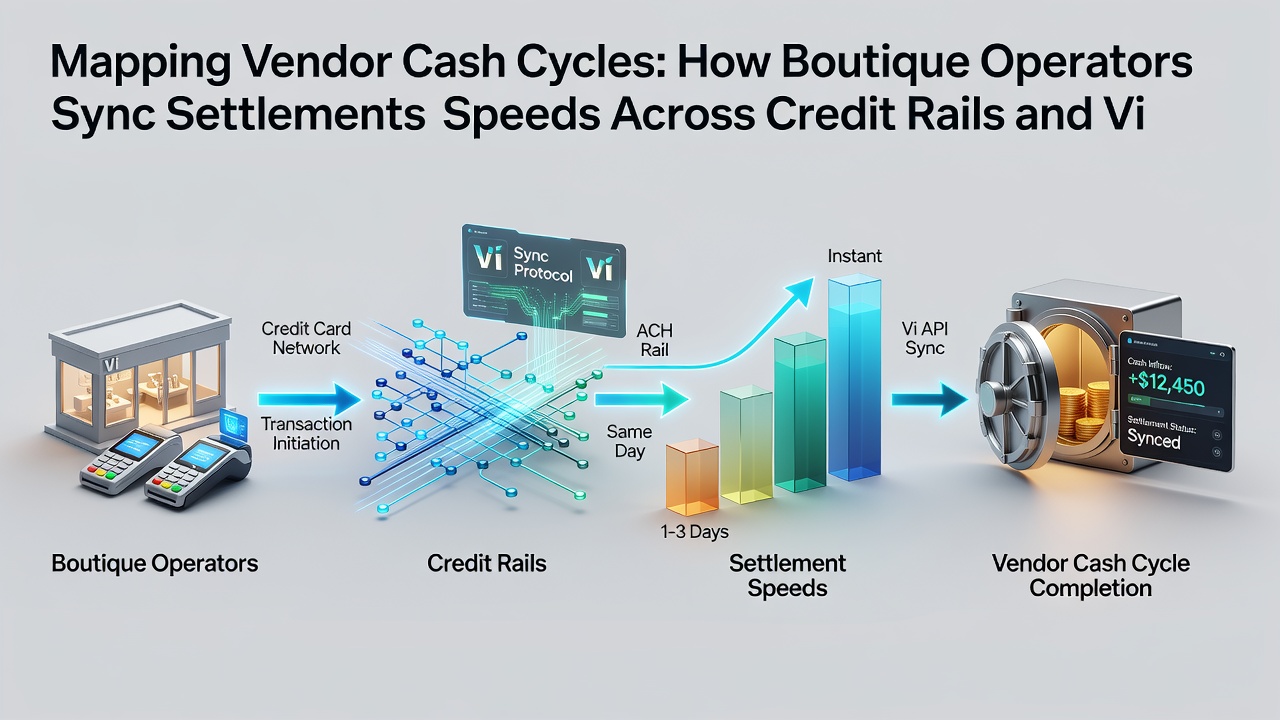

Subscription ecosystems for boutique operators often rely on precise coordination between credit card rails and virtual asset networks to maintain steady cash inflows. Settlement speeds vary widely across these channels with traditional cards typically clearing in one to three business days while certain virtual assets complete transfers in minutes or hours depending on network conditions and confirmation requirements.

Understanding Settlement Variations in Mixed Rails

Operators track these differences closely because mismatched timelines can disrupt inventory replenishment and recurring operational expenses. Data from the Bank for International Settlements indicates that cross-border credit transactions averaged 2.4 days for final settlement in 2025 while stablecoin transfers on major public ledgers frequently reached finality within thirty minutes during the same period. Boutique providers therefore build internal calendars that align expected inflows with upcoming liabilities such as supplier payments and platform fees.

Subscription billing cycles add another layer since charges recur on fixed dates yet actual funds availability depends on processor cutoffs and asset volatility buffers. Many small operators maintain separate ledgers for card batches and virtual asset wallets then consolidate figures weekly to forecast available capital accurately.

Operational Tools for Timing Alignment

Specialized software platforms now offer automated reconciliation that tags each incoming transaction by rail and expected settlement window. These systems flag potential shortfalls when a crypto batch clears faster than anticipated or when card processors extend holds during high-volume periods. Research from the Reserve Bank of Australia highlights that firms using such tools reduced cash flow variance by 18 percent compared with manual tracking methods over a twelve-month review ending in early 2026.

July 2026 saw several boutique subscription services adopt real-time dashboards that pull live data from both card networks and blockchain explorers. The dashboards display countdown timers for each pending settlement alongside projected spend requirements allowing managers to shift discretionary outlays without interrupting service delivery.

Compliance and Risk Buffering Practices

Regulatory expectations continue to shape how operators structure these flows. The Monetary Authority of Singapore requires licensed payment service providers to maintain segregated accounts for client funds regardless of rail which encourages boutique vendors to mirror that separation internally even when self-custodying virtual assets. Such practices help prevent commingling that could trigger extended review periods during audits.

Operators also apply velocity checks and threshold alerts to virtual asset inflows because rapid price swings can alter the effective value of settled amounts. When a crypto settlement arrives ahead of schedule some providers automatically convert a portion into stable holdings to protect against subsequent volatility before the next billing cycle begins.

Case Examples from Niche Markets

One independent wellness subscription service in Canada integrated card processing with stablecoin payouts to international creators. The company routes recurring member charges through established card rails for predictability while compensating content partners via virtual asset transfers that finalize within the same business day. Their internal mapping shows a consistent four-day gap between card settlement and creator payouts which the firm bridges through short-term credit facilities arranged with a regional lender.

Another operator serving specialty food clubs in the European Union documented how blending rails reduced average float time from 3.8 days to 1.9 days across a six-month test period. They achieved this by routing a fixed percentage of volume to virtual asset options on days when card processors reported higher hold rates. Figures published by the European Central Bank in mid-2026 confirmed similar patterns among small payment-service users who diversified rails during seasonal demand spikes.

Conclusion

Boutique subscription operators continue to refine cash cycle mapping as settlement technologies evolve. By maintaining separate visibility into credit rail timelines and virtual asset finality these providers create predictable funding windows that support uninterrupted service and supplier relationships. The practice remains grounded in measurable data from regulatory bodies and industry reports rather than assumptions about future network performance.