Decoding Merchant Pathways: Layered Reviews When Integrating Card Networks and Digital Asset Options

Merchants today trace their operational routes by examining multiple layers of customer feedback and transaction data when they combine established card networks with emerging digital asset options, and this approach reveals patterns that shape payment strategies over time. Observers note that the process involves breaking down each stage of the customer interaction from initial checkout through settlement, which allows businesses to identify friction points across different payment types.

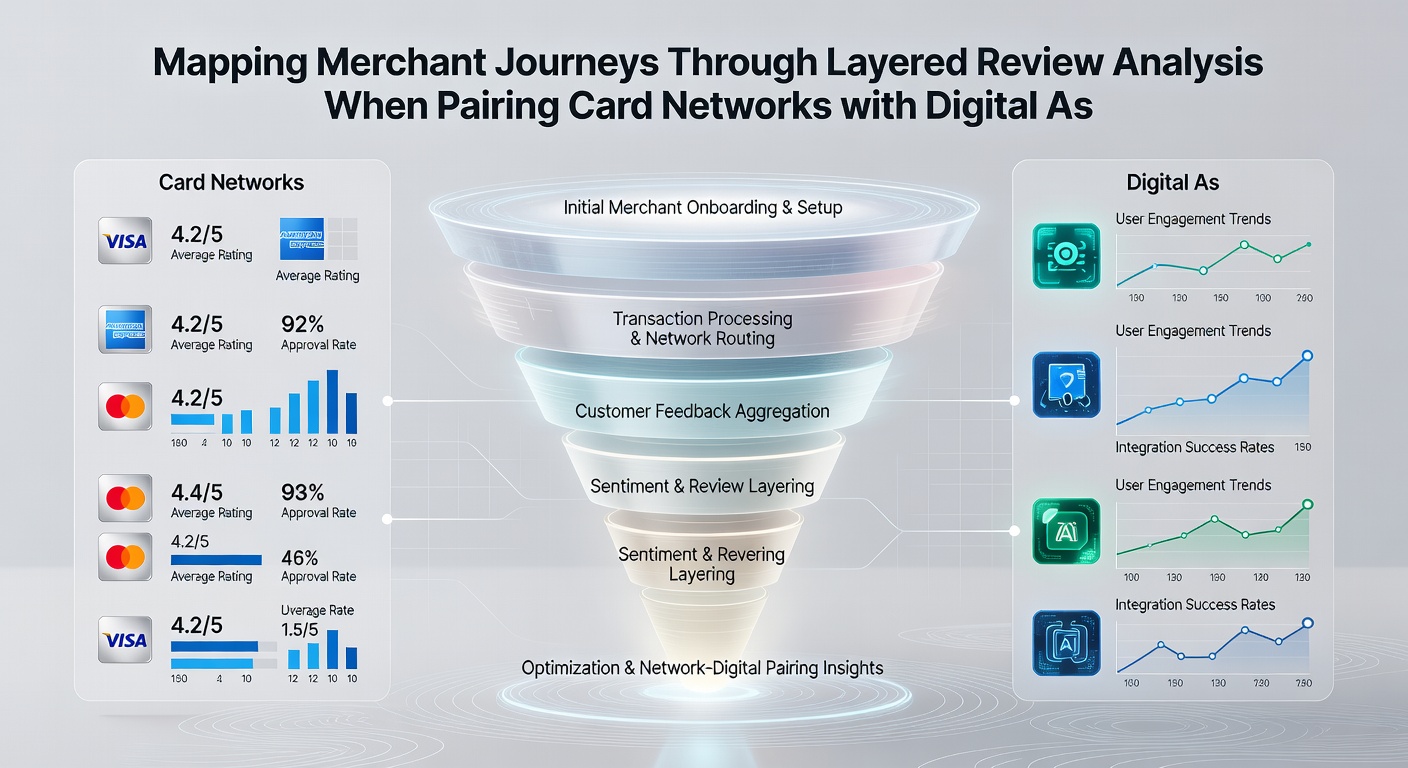

Researchers at various institutions have documented how layered review analysis works by stacking qualitative reviews on top of quantitative metrics such as approval rates and processing times, while quantitative transaction logs get cross-referenced with merchant surveys that capture satisfaction levels at each step. Data from global payment reports indicate that by May 2026 adoption of these combined systems had grown in regions where regulatory clarity around digital assets had improved, particularly in parts of Europe and North America where central banks released updated guidelines on interoperability.

Tracing the Stages of Merchant Journeys

One study revealed that merchants often begin their journey assessment at the point of sale integration, where card network APIs connect with digital wallet protocols, and then they move to post-transaction reconciliation phases that include settlement speed comparisons between traditional rails and blockchain-based transfers. Experts have observed that reviews collected at these stages highlight differences in customer drop-off rates when options for cards versus digital assets appear side by side during checkout.

What's interesting is how businesses stack these insights into visual maps that show progression from onboarding through ongoing operations, and turns out the maps frequently expose hidden costs related to chargebacks in card systems compared with volatility handling in digital asset settlements. According to figures released by the Federal Reserve, transaction volumes involving hybrid setups rose steadily through early 2026 as merchants refined their review layers to include real-time monitoring tools.

Applying Multi-Tiered Analysis Techniques

Layered review analysis breaks feedback into tiers that range from immediate user comments on payment speed to deeper evaluations of security incidents and fee structures over months of operation, and analysts combine these tiers to form a complete picture of journey efficiency. Those who've studied payment ecosystems find that merchants who apply three or more review layers achieve clearer identification of where card network reliability intersects with digital asset flexibility during peak sales periods.

Take one case where experts found that retailers in Canada adjusted their gateway configurations after reviewing six months of data that showed digital asset options reduced overall processing expenses in cross-border sales while card networks maintained higher completion rates for domestic purchases. Research indicates that such adjustments rely on consistent data collection methods that track both success metrics and failure points across the entire transaction flow.

Observing Integration Patterns in 2026

By May 2026 industry reports showed merchants increasingly using dashboard tools that overlay customer review sentiment with network uptime statistics, and this combination helps pinpoint moments when digital asset volatility affects overall satisfaction compared with the stability of established card rails. Observers note that European data from the European Central Bank highlighted similar trends where hybrid pairings improved liquidity management for smaller merchants operating in multiple currencies.

But here's the thing: successful mapping requires regular updates to the review layers because payment protocols evolve quickly, with new digital asset features appearing alongside card network upgrades that alter fee schedules and security protocols. A research paper from an Australian university documented how merchants who refreshed their analysis frameworks quarterly maintained more accurate journey maps than those who reviewed data less frequently.

Connecting Data Sources Across Regions

Trade organizations in Asia have contributed datasets that complement findings from North American studies, revealing regional variations in how merchants weigh the benefits of instant digital asset confirmations against the broader acceptance of card payments. Figures reveal that these cross-regional comparisons strengthen the reliability of layered reviews by accounting for local regulatory environments and consumer preferences that influence journey outcomes.

Conclusion

The practice of mapping merchant journeys through layered review analysis continues to provide structured insights when card networks pair with digital asset options, and ongoing data collection supports refinements that align payment choices with operational realities. Researchers continue to track these developments as systems mature and new interoperability standards emerge across markets.