Retailers Weighing Security Layers and Cost Factors in Mixed Credit Card adn Digital Currency Payments

Retail payment teams face ongoing calculations when they integrate credit card processing with digital currency options, and these evaluations center on specific security requirements that carry measurable expenses. Data from industry monitoring shows that transaction volumes involving both payment types grew steadily through early 2026, prompting merchants to refine their internal review processes rather than rely on static setups. Observers note that decision frameworks often map out multiple protection tiers against projected operational outlays, using models that track encryption standards, authentication tools, and blockchain verification steps alongside fee structures from processors and compliance audits.

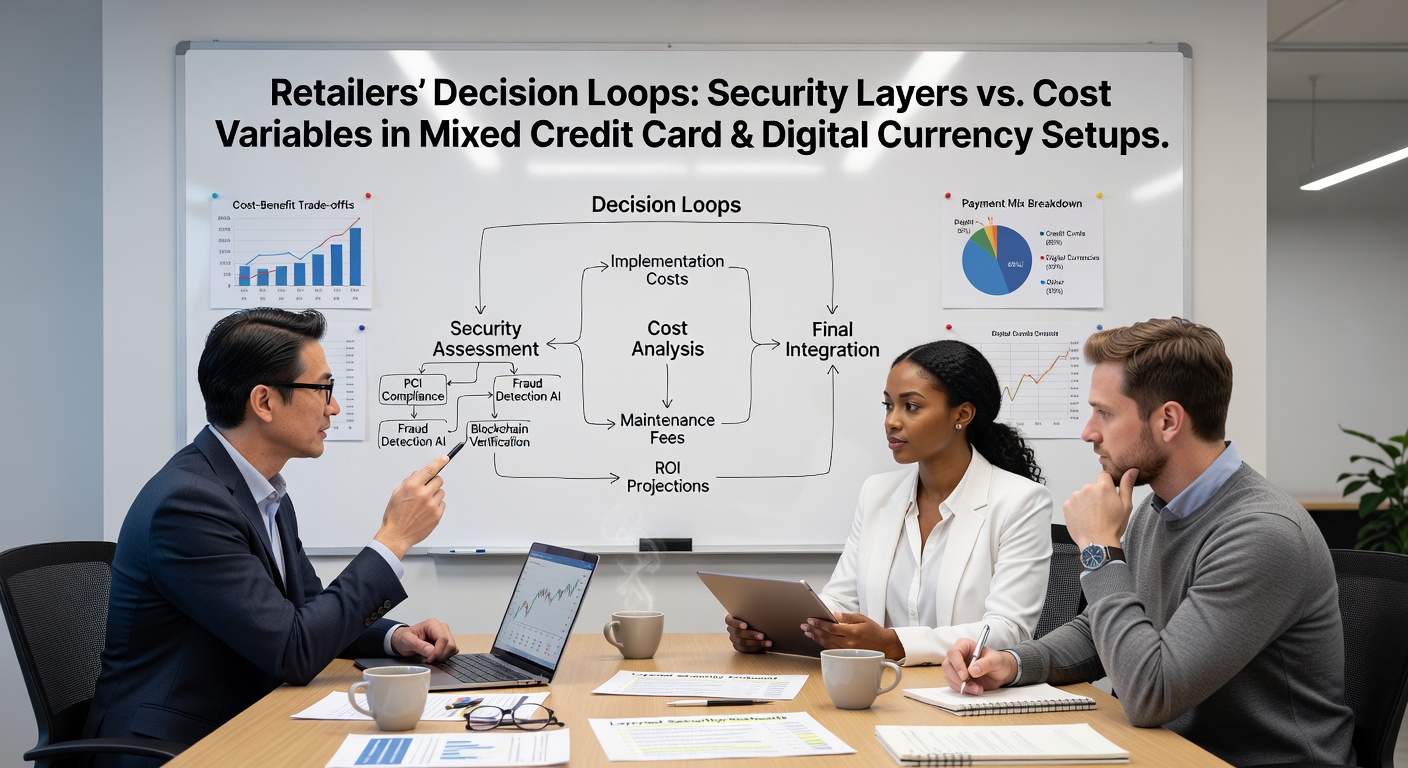

Key Elements in Retailer Assessment Cycles

Security considerations typically begin with established protocols for credit card data, such as PCI DSS requirements that demand regular testing and network segmentation, while digital currency handling adds layers like multi-signature wallets and cold storage procedures. Researchers at academic institutions have documented how these combined environments increase the number of variables in risk matrices, because crypto transactions introduce volatility in confirmation times and exposure to private key management issues. Retailers commonly assign internal teams to run scenario projections that compare breach probabilities, based on historical incident reports, with implementation costs that include software licensing and staff training hours.

Cost variables extend beyond per-transaction percentages to encompass setup fees for hybrid gateways, ongoing monitoring subscriptions, and potential penalties tied to regulatory filings. Figures from a Federal Reserve analysis of 2025 payment trends indicate that merchants operating in mixed systems reported average compliance expenditures rising by 18 percent compared to single-method operations. These calculations also factor in opportunity costs, where delayed adoption of certain security tools might reduce short-term spending yet elevate exposure during high-volume periods such as seasonal sales peaks.

Practical Patterns Observed Across Retail Operations

One mid-sized electronics chain implemented a phased rollout that started with basic wallet encryption for cryptocurrency receipts and later layered in real-time fraud detection shared across both payment streams. The approach allowed the company to measure incremental expenses against reductions in disputed transactions, revealing that shared monitoring platforms lowered overall alert volumes by consolidating data feeds. Similar patterns appear in reports from payment infrastructure reviews, where entities test routing logic that directs lower-risk credit card orders through faster channels while routing digital currency flows through enhanced verification checkpoints.

By May 2026, several retailers had adopted dynamic dashboards that pull live data on both security event logs and cumulative processing fees, enabling quicker adjustments when digital currency network congestion drives up confirmation expenses. Industry groups tracking these deployments note that the dashboards often incorporate external benchmarks, such as average breach remediation costs published by insurance providers, to set internal thresholds for acceptable risk levels. This integration helps teams visualize how adding a secondary authentication step for larger crypto transfers affects monthly overhead without disrupting credit card checkout flows.

Regional and Regulatory Influences on Choices

Payment operators in different jurisdictions encounter varying compliance baselines that shape their internal loops. Guidelines issued by the European Central Bank on digital asset handling, for instance, emphasize traceability requirements that add documentation steps not always present in North American frameworks. Retailers operating across borders therefore maintain separate cost ledgers for each region, adjusting security configurations to meet the stricter standard while avoiding redundant investments. Academic papers examining these cross-regional setups highlight that unified vendor contracts can offset some duplication, though they require upfront legal review fees that factor into the broader decision model.

Additional considerations surface when merchants evaluate insurance coverage for hybrid systems, because policies frequently differentiate between traditional card fraud and cryptocurrency-specific incidents like wallet exploits. Data compiled by trade associations shows that coverage premiums for mixed environments climbed in line with reported attack frequencies on digital asset platforms during 2025. Teams therefore run side-by-side comparisons of premium quotes against the expense of in-house controls, such as regular penetration testing cycles, to determine the point at which external insurance becomes the lower net outlay.

Conclusion

Retailers continue to refine their internal loops by testing incremental security additions against tracked cost metrics in environments that blend credit card and digital currency processing. These structured evaluations draw on aggregated transaction data, regulatory updates, and vendor performance records to guide configuration choices that maintain operational continuity while containing expenses. The patterns documented through 2026 illustrate consistent use of quantitative thresholds rather than fixed rules, allowing adjustments as network conditions and compliance expectations shift.